We are continuously working to improve the accessibility of our web experience for everyone, and we welcome feedback and accommodation requests. If you wish to report an issue or seek an accommodation, please let us know. Foreclosure documents are public records and are recorded with the Clerk and Recorder. Even though you may have cured your default or the foreclosure action has otherwise been withdrawn, the records remain permanently available to the public for viewing.

These types of properties can offer great opportunities for real estate investment. Listing information is from various brokers who participate in the Bright MLS IDX program and not all listings may be visible on the site. The property information being provided on or through the website is for the personal, non-commercial use of consumers and such information may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing.

Search for more Washington foreclosures below:

You may also access various weekly foreclosure reports, review statistical data and see other informational reports by selecting Foreclosure Reports. Foreclosure, the forced sale of a piece of property to repay a debt, is conducted by the Office of the Jefferson County Public Trustee on Deeds of Trust containing a power of sale. Colorado Revised Statutes specify the procedure for conducting the foreclosure, which must be followed exactly. Zillow Group is committed to ensuring digital accessibility for individuals with disabilities.

Below you will find foreclosure listings of foreclosure homes for sale in and near Jefferson county. All our foreclosure listings are pre-screened for accuracy by our team of professionals on a daily basis. Our Jefferson county foreclosures, sheriff sales, short sales and pre- foreclosures, will also include the full contact information for all foreclosed properties including number of bedrooms and baths and price. Due to the federal moratorium on foreclosure evictions during the pandemic, our supply of foreclosure listings is currently low. Please consider looking at other types of properties available here on our website, such as short sales and pre-foreclosures.

Foreclosure Sale Alerts

Some properties which appear for sale on the website may no longer be available because they are for instance, under contract, sold or are no longer being offered for sale. Copyright 2022 Bright MLS, Inc. (/info/mls-disclaimers/#mls_5632) The listing broker’s offer of compensation is made only to participants of the MLS where the listing is filed. The nations leaders in online real estate foreclosure listings information delivery. The number of available foreclosure properties in our database varies with market conditions.

Below you will find foreclosure listings of foreclosure homes for sale in and near Jefferson county. All our foreclosure listings are pre-screened for accuracy by our team of professionals on a daily basis. Our Jefferson county foreclosures, sheriff sales, short sales and pre- foreclosures, will also include the full contact information for all foreclosed properties including number of bedrooms and baths and price. Due to the federal moratorium on foreclosure evictions during the pandemic, our supply of foreclosure listings is currently low. Please consider looking at other types of properties available here on our website, such as short sales and pre-foreclosures.

We are continuously working to improve the accessibility of our web experience for everyone, and we welcome feedback and accommodation requests. If you wish to report an issue or seek an accommodation, please let us know. Foreclosure documents are public records and are recorded with the Clerk and Recorder. Even though you may have cured your default or the foreclosure action has otherwise been withdrawn, the records remain permanently available to the public for viewing.

Search for more Washington foreclosures below:

These types of properties can offer great opportunities for real estate investment. Listing information is from various brokers who participate in the Bright MLS IDX program and not all listings may be visible on the site. The property information being provided on or through the website is for the personal, non-commercial use of consumers and such information may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing.

Some properties which appear for sale on the website may no longer be available because they are for instance, under contract, sold or are no longer being offered for sale. Copyright 2022 Bright MLS, Inc. (/info/mls-disclaimers/#mls_5632) The listing broker’s offer of compensation is made only to participants of the MLS where the listing is filed. The nations leaders in online real estate foreclosure listings information delivery. The number of available foreclosure properties in our database varies with market conditions.

You may also access various weekly foreclosure reports, review statistical data and see other informational reports by selecting Foreclosure Reports. Foreclosure, the forced sale of a piece of property to repay a debt, is conducted by the Office of the Jefferson County Public Trustee on Deeds of Trust containing a power of sale. Colorado Revised Statutes specify the procedure for conducting the foreclosure, which must be followed exactly. Zillow Group is committed to ensuring digital accessibility for individuals with disabilities.

You may also access various weekly foreclosure reports, review statistical data and see other informational reports by selecting Foreclosure Reports. Foreclosure, the forced sale of a piece of property to repay a debt, is conducted by the Office of the Jefferson County Public Trustee on Deeds of Trust containing a power of sale. Colorado Revised Statutes specify the procedure for conducting the foreclosure, which must be followed exactly. Zillow Group is committed to ensuring digital accessibility for individuals with disabilities.

These types of properties can offer great opportunities for real estate investment. Listing information is from various brokers who participate in the Bright MLS IDX program and not all listings may be visible on the site. The property information being provided on or through the website is for the personal, non-commercial use of consumers and such information may not be used for any purpose other than to identify prospective properties consumers may be interested in purchasing.

JeffersonForeclosure Listings

Below you will find foreclosure listings of foreclosure homes for sale in and near Jefferson county. All our foreclosure listings are pre-screened for accuracy by our team of professionals on a daily basis. Our Jefferson county foreclosures, sheriff sales, short sales and pre- foreclosures, will also include the full contact information for all foreclosed properties including number of bedrooms and baths and price. Due to the federal moratorium on foreclosure evictions during the pandemic, our supply of foreclosure listings is currently low. Please consider looking at other types of properties available here on our website, such as short sales and pre-foreclosures.

We are continuously working to improve the accessibility of our web experience for everyone, and we welcome feedback and accommodation requests. If you wish to report an issue or seek an accommodation, please let us know. Foreclosure documents are public records and are recorded with the Clerk and Recorder. Even though you may have cured your default or the foreclosure action has otherwise been withdrawn, the records remain permanently available to the public for viewing.

Search for more West Virginia foreclosures below:

Some properties which appear for sale on the website may no longer be available because they are for instance, under contract, sold or are no longer being offered for sale. Copyright 2022 Bright MLS, Inc. (/info/mls-disclaimers/#mls_5632) The listing broker’s offer of compensation is made only to participants of the MLS where the listing is filed. The nations leaders in online real estate foreclosure listings information delivery. The number of available foreclosure properties in our database varies with market conditions.

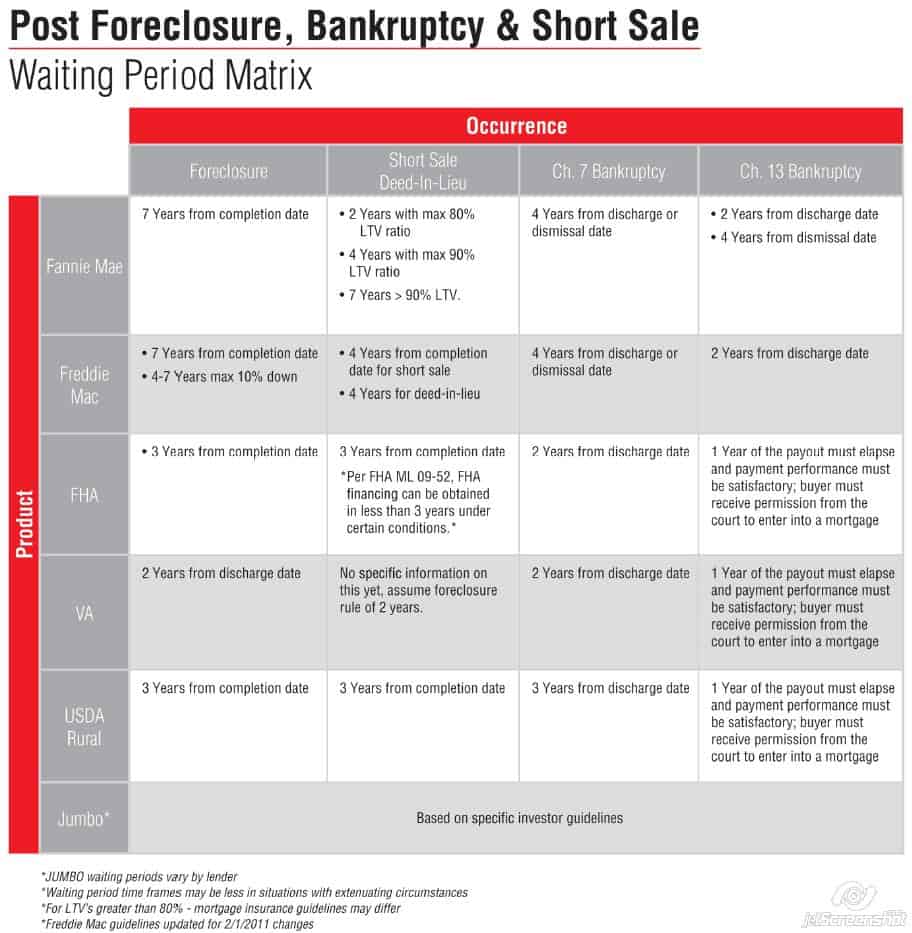

It's one of the greatest civil rights injustices of our time that low-income families can’t access their basic rights when they can’t afford to pay for help. Combining direct services and advocacy, we’re fighting this injustice. Your Chapter 7 bankruptcy will stay on your credit report for ten years with all three credit bureaus, but your score can start improving as early as your discharge date. The other type of bankruptcy - Chapter 13 bankruptcy, stays on your credit report for only 7 years after filing bankruptcy. This waiting period can be longer if you’ve filed multiple bankruptcy cases.

Having a waiting period in place gives you the chance to rebuild your credit score and show that you have the ability to take on and maintain mortgage payments. FHA loans are mortgages backed by the Federal Housing Authority, designed for people who may have trouble getting a conventional loan because of a poor credit history or income. FHA loans have easier credit requirements and lower down payments. There are also nonprime lenderswho are willing to finance your home immediately after a chapter 13 bankruptcy discharge. They will look at your credit scores to determine what the down payment and interest rate will be. However, to even be considered for a mortgage loan request, the bankruptcy must first be discharged.

What Are the Pros and Cons of a Leaseback for Homeowners?

If the trustee sells the house, it will be sold to the highest bidder. The trustee then takes the remaining amount from the sell of the house to pay creditors. After all creditor payments and trustee fees are covered, any remaining funds would go to Linda .

Bankruptcy will impact your credit history and your credit score, which in turn impacts how soon you can get a line of credit after bankruptcy. A Chapter 7 bankruptcy will stay on your credit report for up to 10 years, while a Chapter 13 bankruptcy will stay on your credit report for up to seven years. The impact on your credit score depends on several factors, including your score before bankruptcy. For example, if you had a high credit score, you should expect to see a bigger drop than someone with a lower score who had existing negative marks on their credit report.

Buying A House After Chapter 7 Bankruptcy Faq

Make sure your broker and lender knows about the bankruptcy early. Lenders ask for statements to prove that your last six months repayments have been on time. When you are discharged from bankruptcy, it means that youre no longer bankrupt. Any restrictions that were in place during the bankruptcy term, such as not being able to travel overseas or limits on the amount of assets you can own, no longer apply. Filing for bankruptcy doesn’t have to put a damper on your home buying dreamat least not for long. Lenders have eased requirements, opening the door for bankruptcy filers to get back into a home sooner than in the past.

Conventional loans are private loans made by banks and mortgage companies without government backing. In theory, this means that conventional loans don’t need to follow the government waiting period. However, most of these loans are sold to either the Federal National Mortgage Association or the Federal Home Loan Mortgage Corporation .

What Are My Chances Of Getting A Mortgage After Bankruptcy

There are both federal and state exemptions available, although Maryland does not allow those who file bankruptcy to claim the federal exemptions. You will need to use the state exemptions if you move forward with Chapter 7 bankruptcy in Maryland. To qualify for an FHA loan, you’ll need to show that your credit has been improved and that you haven’t taken on additional debt since your bankruptcy. While the bankruptcy dinged your credit and affects it for seven years, most of the problems hit your credit in the time leading up to the bankruptcy filing. Getting approval for any type of credit after a bankruptcy is challenging. However, with the right combination of bankruptcy seasoning and steps to rebuild your credit, you can look for a home equity loan in as little as two years.

There are a lot of balls to juggle when getting a mortgage after bankruptcy. Besides the variety of mortgages available, all with their own rules, there are also different types of bankruptcy. Both factor in to how long you have to wait before you can apply for a mortgage after bankruptcy is discharged.

How Far Can You Fall Behind On Your Mortgage

For FHA loans, the waiting period is 2 years after your bankruptcy discharge. If, however, you are able to prove extenuating circumstances, you may qualify for the 12-month exception. For this to be approved, you’ll need to show that you filed bankruptcy through no fault of your own and that you’ve handled your finances well since that time.

What happens at the end of the lease, notably if you can repurchase the property. Instead of 80% of the value of the house, the Loan to Value ratio, they may lend a lesser amount.

Home Equity Loan After Chapter 7

Because a bankruptcy discharges debts that became overwhelming financially, lenders are reluctant to give a loan for consolidating other surmounting debts such as credit cards. The amount of time it takes to get cash will vary depending on the applicant’s respective financial circumstances and the Lending Partner’s current volume of applications. Under a Chapter 7 bankruptcy, you can keep certain “exempt” assets, like clothing, household goods and other personal belongings.

The good thing is that with the right help and advice you can get a mortgage with a similar LTV and interest rates to what other borrowers get. If you are forced to file for bankruptcy following a foreclosure, know that you may still qualify for another mortgage in the future. In most cases recovering from foreclosure and getting approved for another mortgage can take seven years. However, each lender has different time frames in which it will reconsider someone who has filed for bankruptcy. When you get a mortgage, you should learn what not to do in order to save time and money while getting approved. Millennials can rest assured that we review everything they need to know about purchasing a home.

For HELOCs borrowers must take an initial draw of $50,000 at closing. Subsequent HELOC draws are prohibited during the first 90 days following closing. After the first 90 days following closing, subsequent HELOC draws must be $1,000 or more . Before allowing your HELOC to be discharged in Chapter 7, it’s a good idea to communicate with your HELOC lender and see if they’re willing to work with you. You may be able to negotiate a payment plan that fits within your budget and allows you to keep your home. When you’re ready to start looking for a new home, it’s a good idea to get prequalified first.

Such extenuating circumstances could apply if you were forced into bankruptcy due to a serious illness or major job loss or income reduction. So youre in the process of re-establishing your credit and have put yourself in a better place to take on a mortgage, but dont run out to your bank or mortgage agent just yet! Michael and Bev explain that a mortgage is possible at a 5% down but you will pay a cost in terms of mortgage insurance.

HELOC Bankruptcy Options

It may take a while, but eventually, you can get a HELOC after Chapter 7 bankruptcy has been discharged. You may be able to deduct the interest on the debt on your income taxes. Interest paid on home equity funds used for home improvements may be tax-deductible.

If a mortgage loan debt was discharged through a Chapter 7 bankruptcy, the mandatory waiting period after a bankruptcy discharge date is the waiting period start date. The date of the foreclosure, deed in lieu of foreclosure, and short sale after the bankruptcy do not matter. There is a four-year waiting period after the discharge date of the bankruptcy to qualify for a conventional loan. Things may be slightly different in chapter 13 bankruptcy but being allowed to obtain a home equity loan during the process is still very unlikely.

That will tell you the appropriate purchase price range to look for and will give you an idea of what your monthly payment will be. A big reason to do a leaseback is the fact that it will get you all of the equity in your home. With a bankruptcy on your record, you will probably qualify for less than that. If home sales in your market are strong, you’d like to take advantage of that and sell your home now.

If you have made at least 12 months of payments toward this plan, you may be eligible if the trustee or judge overseeing your bankruptcy approves the application. Like Chapter 7 bankruptcy, you need to meet financial and income standards to be approved. Chapter 13 bankruptcy is often called “reorganization” bankruptcy and usually involves a repayment plan that can help you pay debts without selling property. If you satisfactorily completed the repayment plan, you can be eligible for a VA loan.

What Are the Pros and Cons of a Leaseback for Homeowners?

LendingTree does not include all lenders, savings products, or loan options available in the marketplace. LendingTree is compensated by companies on this site and this compensation may impact how and where offers appear on this site . Selling your home and leasing it back from the buyer will get you all of your equity quickly with no debt payments.

If the trustee sells the house, it will be sold to the highest bidder. The trustee then takes the remaining amount from the sell of the house to pay creditors. After all creditor payments and trustee fees are covered, any remaining funds would go to Linda .

How Foreclosure Prolongs a Mortgage Waiting Period

To qualify for a bankruptcy in under two years, youll need to be able to show that your bankruptcy was necessitated by extenuating circumstances and unlikely to reoccur. You will also need to demonstrate that you can manage your finances since your bankruptcy occurred. The general rule is to wait two years after your Chapter 7 bankruptcy is discharged before you can reasonably expect to qualify for a home loan. If you’ve been bankrupt previously, your name is placed on the National Hunter database. This is a database containing everyone who’s been bankrupt – even after theyve been discharged. Regardless of whether you own up to it, a lender will be able to find you on this database.

This can be a huge benefit to you as you rebuild your financial life. Even though the ability to declare yourself bankrupt is found in federal law, the states have a lot to say about how your property is affected. Other banks may insist that you wait until 5-7 years afterward, and others will not approve you unless the bankruptcy is off your report entirely. To keep from losing your home, you are also not allowed to access your home’s equity during the bankruptcy process.

Can Bankruptcy Stop Your Eviction?

Speak to an experienced bankruptcy lawyer from the Van Horn Law Group. Some banks might consider giving you a home equity loan as soon as three years after bankruptcy, but again, it mostly depends on how you work to repair your credit during that time. Other banks may insist that you wait up to 5-7 years after that, and others won’t approve you unless bankruptcy is entirely out of your report.

A bankruptcy discharge is an order from a bankruptcy court that releases you from any liability on certain debts and prohibits creditors from attempting to collect on your discharged debts. All of the above waiting periods can be impacted, and potentially increased, if your bankruptcy included a foreclosure. In that case, the FHA loansâ waiting period increases to 3 years and conventional loans increases to 7 years. Both VA and USDA loans remain the same, at 2 and 3 years, respectively. Proving extenuating circumstances can reduce the waiting period.

Can I Get A Mortgage Loan After Chapter 7

Your eligibility for a Chapter 7 bankruptcy is based on income. You generally qualify for a Chapter 7 bankruptcy if you’re below the median income level for your state. If your income is above the median level, a “means test” is applied to determine your ability to pay back the debts you are trying to dismiss. You don’t have to give up on the American dream of becoming a homeowner just because you filed a bankruptcy. You can absolutely get a mortgage after a Chapter 7 bankruptcy. The larger question is when are you able to qualify for a mortgage, which can vary based on the type of loan you are pursuing.

Start by checking websites like Realtor.com and Zillow.com when valuing your home before bankruptcy.Subtract the mortgage balance. The amount necessary to pay the loan and any liens in full.Find out how much equity you can exempt. The homestead exemption covers equity in a home in which you reside. The wildcard exemption might cover an additional amount, but not all states offer a wildcard exemption or allow filers to use it for real estate. However, if you have nonexempt equity, you’ll have to pay an equivalent amount toward your general unsecured debts through your repayment plan.

Learn the ins and outs of a home equity loan vs. a home equity line of credit to decide which option is best for your financial goals. Every homeowner who applies for a HELOC or home equity loan will need to meet lender requirements. The sale of the property will be easier than selling to another homeowner. There will not be any brokers or lenders involved, so there is less paperwork and fewer inspections.

Your creditors cannot contact you after you file for bankruptcy, nor can they attempt to collect payment for medical bills, credit card debts, personal loans, or other types of debt. The filing of bankruptcy is a life-changing experience, but there are some things you should not do before filing. A large number of people try to avoid bankruptcy laws by concealing or giving away assets that should be disclosed in a bankruptcy filing. Approximately 5% of people who file for bankruptcy do so by themselves. If you give your loved one a gift of good will with the understanding that they will return it later, you are not allowed to give it away. Giving your car to a family member before filing for bankruptcy is a simple way to lose it.

FHA Guidelines On Mortgage Part of Bankruptcy

This means that if the value of your house is excluded and you are allowed to keep it, the condition is that the value remains in the house and the owner is not allowed to access it in cash. You’ll pay closing costs that will increase your loan balance or require cash. Closing costs typically range from 2% to 5% of the loan amount, which you can pay upfront or wrap into your loan.

A leaseback is when you sell your home to an investor and then lease it back from them as their tenant. If you are looking for a HELOC after bankruptcy, you may not get the maximum LTV, which means that you won’t be able to use as much of your equity. However, other investments may give you a higher return than annual property value appreciation.

What Is A Hero Mortgage Loan

There are a lot of balls to juggle when getting a mortgage after bankruptcy. Besides the variety of mortgages available, all with their own rules, there are also different types of bankruptcy. Both factor in to how long you have to wait before you can apply for a mortgage after bankruptcy is discharged.

The short answer to your question is that someone else cannot use your income to help them qualify for a mortgage. Even if your income is deposited into the same bank account as the person who applies for the mortgage, the lender does not consider the income when the person applies for the loan. If you’ve explored your options and decided that a personal loan is right for you, it’s wise to shop around to find the right loan. Consider personal loans from SoFi, which offers loans of up to $100,000 with no fees.

The process of giving full title to a husband requires that the wife sign specific forms before the refinance or purchase transaction closes and the trust deed is recorded with the county. Although your husband may be the breadwinner of the family and earns a large income, he is of no value to the loan if his credit is so bad that it doesn't meet the lender's minimum credit standards. In this situation, it makes more sense for your husband to repair his credit, raise his score and pay any judgments or collections hindering his mortgage qualifying. Bad credit increases the risk of default, making your household a high risk for a mortgage lender, therefore raising your interest rate. If you're married, your spouse's credit score or debts could hurt your chance to qualify for a mortgage loan.

Re: Can I use my husbands income to qualify for a mortgage without adding him to the loan?

Borrowers may receive funding as quickly as the same day it is approved. If you have a limited or no credit history, consider taking some time to improve your credit before applying for a loan. If you want to borrow a large amount of cash but need to prove additional household income, your spouse may be able to help. You cannot simply list a spouse’s income with, or instead of, your own if you apply in your name alone. However, you can list their income if your spouse agrees to become a “co-borrower” on the loan.

Now, if one spouse doesn’t meet these requirements – say this spouse doesn’t have 2 years of W-2s – then it might make sense to leave this spouse off the mortgage. If your spouse isself-employed, they will usually need 2 years of business returns . If your spouse is unable to provide this documentation – for instance, if they have only been in business for a year – then it may make sense to leave this spouse off the loan. There are a lot of things to consider when you’re getting ready to buy a house. But if you’re married, one that you might not have thought about is whether you and your spouse should both be on the home loan.

How many times your salary can you borrow for a joint mortgage?

If a husband and wife obtain loan approval jointly, using both of their credit scores, combined income and assets to qualify, the lender generally requires both borrowers remain on title as joint owners. A wife who quits her claim to real estate, while remaining responsible for the loan's repayment takes on the financial obligation without the benefits of ownership. A husband who intends to own real estate separately and qualifies to do so on his own income can obtain the loan by himself. Non-borrowing spouses, also known as non-purchasing spouses in FHA terms, are subject to certain rules when left off of a mortgage loan in a community property state. Community property law, as opposed to the common law of most states, makes homes purchased within a marriage equal property of both spouses. Likewise, debts acquired during the marriage by one spouse are also the responsibility of the other spouse.

The lender also needs to see that your husband had the funds in his account for a minimum amount of time and that the money did not come from a credit card or another third party. The letter must state the donor's name, his relationship to you and the date and amount of the gift. It also must include a statement that the funds are indeed a gift requiring no repayment.

What do banks look at when applying for a personal loan?

Indeed, for many, a single income stream from one employer is all they have — and all they need. When someone sets up an IRA, there is no requirement that the spouse of the account holder be named as beneficiary or even that the spouse consents to the designation of other beneficiaries. Here are some of the financial rules for stay-at-home spouses, defined as someone working on the home front but not drawing a paycheck.

Your mortgage lender will look closely at your credit history, your debts, cash on hand, and income to gauge affordability. California and a few other states are community property states. Under their laws, any debts or income incurred after you're married belongs to both spouses, including most assets acquired.

Credit & Debt

They can be either fixed, staying the same for the mortgage term or variable, fluctuating with a reference interest rate. It protects against predatory lending to people who have little chance of repaying their mortgages. Many first-time home buyers won’t have to worry much about multiple income sources.

Most home loan programs require two years of consecutive employment or consistent income, either with the same employer or within the same field. This is a sign of stability, indicating that your annual income will likely remain reliable for at least three years after closing on your home purchase. It doesn't matter that they are only $1500 total - even if a collection is only one dollar it drops your scores a bunch . Go to the rebuilding forum to get stategies for those specific collections.

You can't combine your income and just use your scores, if you use his income he has to be on the loan. Also, your debt to income is high but not too high to qualify... However since you have excellent credit scores, and if you can document 2 months of reserves you'd have a pretty good chance of qualifying on your own. A mortgage lender might also need to pull your non-borrowing spouse's credit if you live in a community property state.

If you’re the only one on the mortgage, theunderwriterwill only look at your stuff, right? Here are a few things to know if you’re getting a mortgage without your spouse. As a self-employed borrower, be mindful that too many business deductions on your tax return can reduce your qualifying amount.

Complications with a Joint Auto Loan

Although there is no set time frame, the custom within the real estate industry is that mortgage pre-approval is valid for between 90 to 180 days. Make sure to ask your lender how long your pre-approval lasts, or look for this expiration date on your pre-approval letter. Mortgage pre-approval is a statement from a lender who’s thoroughly reviewed your finances and decided to offer you a home loan up to a certain amount. Pre-approval is a smart step to take before making an offer on a home, because it will give you a clear idea of how much money you can borrow to pay for a house.

Bankrate has partnerships with issuers including, but not limited to, American Express, Bank of America, Capital One, Chase, Citi and Discover. Megan Foukes is a recent graduate from Indiana University who graduated with a bachelor’s in journalism. Megan works as a content writer for Auto Credit Express and contributes to several automotive and finance blogs. Hearst Newspapers participates in various affiliate marketing programs, which means we may get paid commissions on editorially chosen products purchased through our links to retailer sites. When you receive your report, review it closely and make a note of any incorrect information.

Can I use my credit and someone else's income to buy a house?

Having the ability to list household income on a credit card application can be a real game-changer for families—particularly those with one parent who stays at home. If one spouse earns $20,000 per year and another earns $150,000, both have the same access to credit thanks to the ability to use household income during the application process. You can combine incomes for a car loan with your husband or wife.